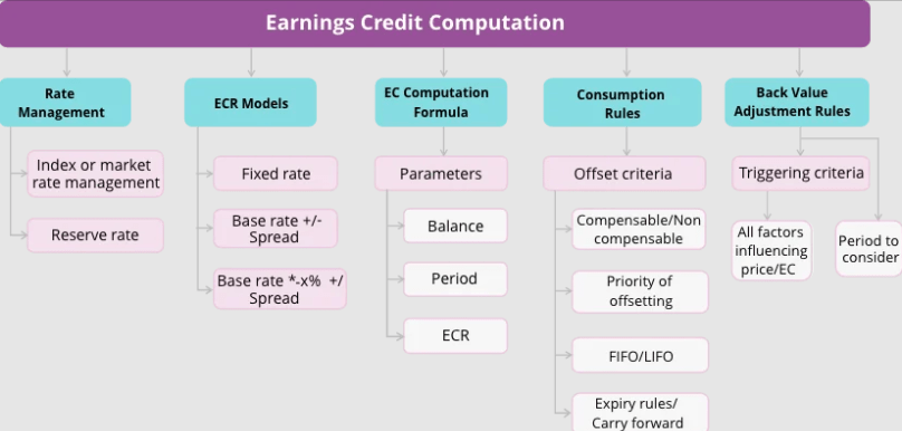

For each period, the balance on which earnings credit is calculated is also a variable. It may be computed based on:

In traditional Account Analysis, the number of the customer’s balances that were required to be held in reserve by the bank were subtracted so earnings credit would not be applied. Additional changes made by the Federal Reserve have made this reduction unnecessary. However, some banks may still want to continue the reduction.

While banks typically generate account analysis statements monthly, the earnings credit may need to be calculated at a different frequency - daily, weekly, quarterly, annually or based on a contractually agreed billing schedule.

The frequency may also need to change from time to time.

Services offered by banks can typically be offset by earnings credit. These services are referred to as balance compensable or analyzed. For a variety of reasons, a bank may have certain services that cannot be offset with earnings credit. These services are referred to as non-balance compensable, or hard charges.

If the earnings credit in an analysis period exceeds the total of the analyzed service charges, the account is “in excess”. Typically, the excess earnings credits are lost, but banks can offer to carry forward excess earnings, giving additional benefit to the customer’s balances if there is seasonality to their cash flows.