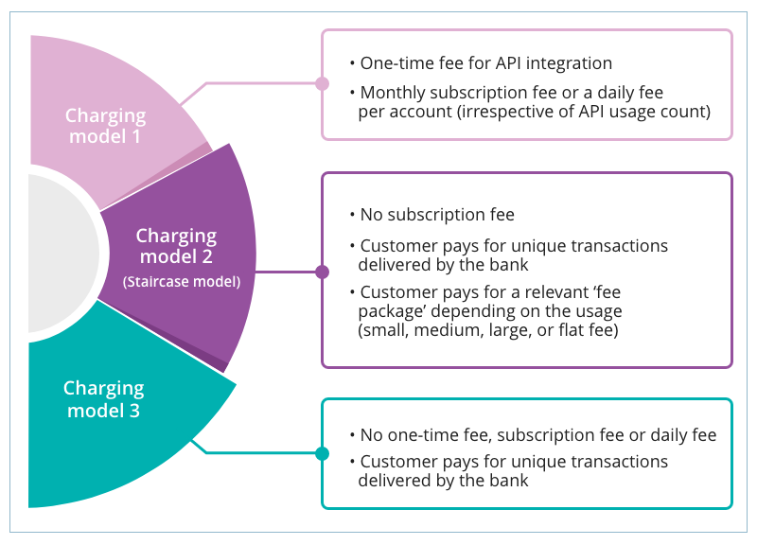

A third charging mechanism option is one in which the customer pays for unique transactions delivered by the bank when the account information API is utilized. There is no one-time fee, subscription fee or daily fee. This is similar to the above charging model, but customers are not segregated and charged as per the fee package.